The Ultimate Guide To Money While Backpacking

This post may contain affiliate links. If you make a purchase using one of these links, I may receive a small reward at no extra cost to you. See my Disclosure Policy for more information.

Short trips abroad are rather easy to organize money-wise, but long-term travel presents unique challenges.

You cannot carry a thick stack of cash – security precautions and customs limits prevent that. It’s not convenient either.

But managing money while backpacking is not rocket science.

I will tell you what I do to:

- Minimize the fees I pay.

- Increase security and always have a backup plan.

- Be prepared to travel to any country.

- Avoid scams.

Set up low-fee bank accounts

Most traditional banks are horrible for traveling. They charge an arm and a leg for each ATM withdrawal, extra for paying in a foreign currency, and sometimes even a percentage of each transaction you make abroad.

My traditional bank in Bulgaria charged me 5 EUR + 2% of the amount every time I withdrew foreign currency from an ATM. That’s exorbitant. I also had a 3 EUR monthly fee. I closed my account for good.

On the other hand, there are fintech banks. They charge little to no fees (up to a limit) and give customers more utility. Practically all such banks offer free accounts and charge no monthly fees.

This is why I recommend you set up at least 3 such accounts. Things happen, cards get declined, lost, or damaged. Also, having more than 1 gives you a bigger fee-free allowance.

Try to have at least 1 VISA and at least 1 Mastercard. Some places don’t accept one or the other.

Here’s what I use.

Revolut is my main bank and payment tool. They have a bank license, so you’re covered up to 100,000 euros (or equivalent) under a Deposit Insurance Scheme.

I use the free plan as it offers fee-free monthly withdrawals of up to ~230 EUR and fee-free currency exchange of up to 1050 EUR.

Paid plans come with various perks and could be worth it depending on your traveler profile. For short trips of up to 90 days, the Premium plan is a big value for its travel insurance.

Wise is an amazing fintech with super transparent fees!

When exchanging money, they use the Interbank rate and charge a small, very competitive fee. Sometimes it turns out to be cheaper than all other alternatives!

Wise also offers up to 200 eur in free ATM withdrawals.

Best of all, you can open local accounts in many currencies, including USD, GBP, AUD, and EUR, where you can receive money as if you were a resident of that country. It’s a must-have for digital nomads!

Monese is one of my backup banking apps.

Unfortunately, the free plan does not offer anything without a fee anymore.

However, the Classic Plan is affordable and offers up to 900 euros fee-free ATM withdrawals! If you need to withdraw that much, it’s usually cheaper to pay for the plan than to withdraw and pay a 2% fee on it.

Curve is an app that combines all of your existing cards into one.

Simply link any card to Curve and get charged in its local currency.

It adds immense value if you link a traditional bank card, but not so much if you already use a fintech bank.

Since it has low fee-free limits on the free plan, I mostly use it as a backup card.

Other fintech banks, depending on your country

If you’re from the UK, you can try Starling Bank. It is as good (if not more) than any traditional bank, offers all sorts of accounts and perks, and has minimal fees.

Another UK-only fintech is Monzo.

Those from the US should go for Charles Schwab. This bank is notorious for refunding all ATM withdrawal fees, so you don’t have to worry about which ATMs to use.

Those in Europe (but not all countries) can also create an account on N26. Accounts are free, but ATM withdrawals in a foreign currency are charged at 1.7%.

Always carry some USD or EUR

Never go abroad without some hard cash. The two best currencies to carry are the USD and the EUR, because they are accepted pretty much everywhere around the globe.

GBP, AUD, SGD, CHF, JPY, and a few others are good enough. If you have such, exchange just a little into USD and keep the rest as is. Otherwise, double exchanging will cost you too much in margins.

In any case, you must always have a couple of hundred pristine, new edition, high-denomination USD/EUR banknotes hidden somewhere on your person or in your backpack.

I know of backpackers who lost their wallets and then looked for someone to transfer money to and get cash back. Others are unlucky with ATMs, and their cards get swallowed. Things happen. Hard cash is your lifeline.

I also carry some small banknotes (10s and 20s) for when I arrive at an airport without a fee-free ATM. I exchange just 1 banknote at the big-margin exchange bureaus at the airport, go to the city center, and then withdraw from a better ATM or exchange at a better bureau.

Last but not least, some countries have a visa on arrival, for which they require USD and only USD. Any other currency (sometimes even the local currency!) is either rejected or exchanged very poorly. Laos and Cambodia are such examples.

What to do when you arrive in a new country

Buy and do as little at the airport as possible. Airports are the worst place for anything money-related.

Exchange bureaus have awful rates, ATMs are scarce and often only of the worst kind, and everything is overpriced.

Apart from that top tip, here’s my simple process for tackling a new country.

1. Research the ATMs with no withdrawal fees

Some ATMs charge more than others. Knowing which ATMs to use to withdraw money will save you hundreds of dollars in fees in the long run.

Fee-free ATMs are one of the main things I note in my money guides. I have covered over 20 countries already.

Another source for such useful knowledge is the ATM Fee Saver app, which shows you the best ATMs in over 50 destinations.

If a country isn’t covered in either place, do some digging online. Forums like Reddit and Tripadvisor tend to be a treasure trove for such knowledge, as travelers share their first-hand experiences there.

2. (If no fee-free ATMs) Exchange just enough to get to the city center

If the ATMs at the airport charge a fee and I know I can find one without a fee in the city, then I exchange 10 or 20 USD or EUR. Just enough to get to the city center by whatever transport options exist (bus/train/taxi).

That’s also enough cash for a snack and a drink, too – very important, given that I minimize my consumption at airports and on the plane.

3. Find the best ATM in the city

I prioritize withdrawing from an ATM over exchanging cash as long as:

- I am within my fee-free withdrawal limit (having several bank accounts helps with that)

- An ATM that doesn’t charge a fee exists in the country

Then it’s a matter of finding and visiting it.

If possible, withdraw from an ATM during working hours on a weekday, at a machine connected to a bank. This way, if your card gets swallowed, you can request assistance and retrieve it more easily.

4. Get to know the denominations and colors of the money

As a foreigner, you’re prone to getting scammed. Get accustomed to the different banknotes, coins, their colors, and signs, to minimize the risk of becoming a victim.

Many different scams exist around the world. Spend a few minutes organizing your new banknotes and coins, so you get accustomed to their look and feel.

10 top money tips for travelers

These are my tricks for saving money for long-term travelers and budget backpackers. Sourced from years of traveling and the unstoppable desire to make money last longer, increase security, and avoid scams.

1. Don’t buy foreign currency before you arrive

The best exchange rates for any foreign currency are in the country where it is used.

It’s basic economics – abundant supply leads to a drop in price. In the case of exchange rates, this means smaller margins.

So next time you go abroad, don’t buy the currency at home – bring your currency (unless it’s a poorly traded one) and exchange it after you arrive.

2. Don’t withdraw/exchange too much

If you have leftover money at the end of your stay, you will have to exchange it back to your currency, thus costing you money.

Additionally, the less money you have on you, the safer it is.

Unless you incur a fee per withdrawal (from the ATM or your bank), it’s better to take money from the ATM little by little every few days.

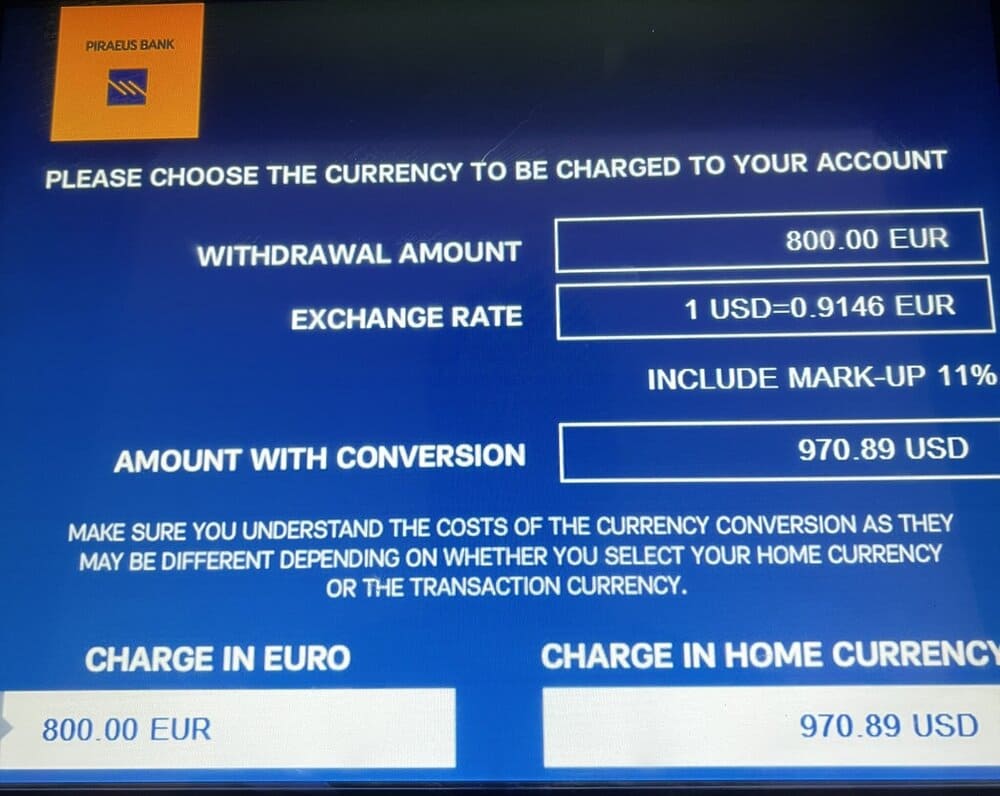

3. Never accept Dynamic Currency Conversion (DCC)

Some ATMs will ask you if you want to pay in the currency of the card you’re using. It may seem like they are doing you a favor.

“Oh, so nice of you to show me the amount in a currency I recognize.”

It’s a trap.

The exchange rate is horrendous. You are getting scammed.

Always, always, always reject such propositions. Never accept DCC.

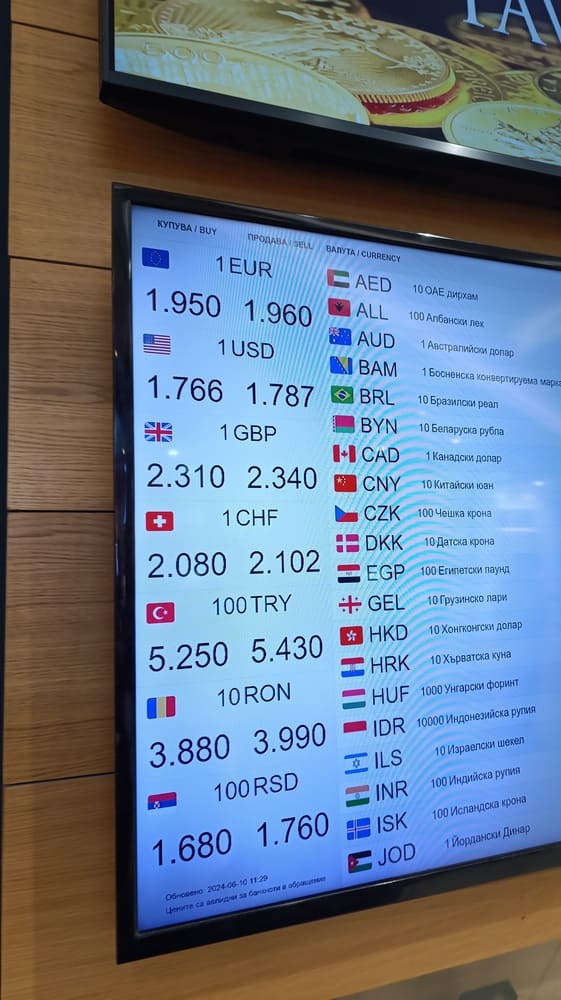

4. Look at the spread to quickly find out if a currency exchange offers good rates

Instead of comparing buy/sell rates between exchange bureaus, a quicker way to know if a bureau is good is to just take note of the spread.

The spread is the difference between BUY and SELL for a currency. The larger it is, the worse the rate.

For example, the USD rate has a spread of ~1.1% which is quite good.

Using this technique, you don’t need to know the midmarket rate for any currency pair. Just note the spread – if it feels too big (a difference of 3% or more), then the exchange bureau is bad.

5. Learn the multiple of your currency

Another “quick maths” tip is to learn how to estimate the cost of things in your currency.

Say you’re in Thailand and use USD as your main currency. You check the rate to find out that 100 THB is around 3 USD. Your “multiple” is 3 with all the zeroes ignored.

If something costs 400 THB, then 3*4=12 USD. If it costs 240, then a quick calculation shows that it’s 2.4*3=7.2$.

For the sake of another example, imagine you’re now in Vietnam where 100.000 VND is 4$. Your multiple is now 4 with all the zeroes ignored. If something costs 350.000 VND, then a rather quick calculation later, you will get to the price of 14 USD.

6. Pay by card unless there is a fee

While traveling long-term, hard cash is valuable. Not because it has more value, but because it usually costs fees to get hold of it.

Pay by card whenever possible, as long as you’re not paying an additional fee for it.

7. Get cash before going to an island

Islands are isolated, making everything more expensive.

Smaller islands may not even have ATMs.

Get enough cash on the mainland before sailing to a tropical paradise.

This does not apply to big islands like Bali and Luzon, but rather to smaller islands like those off the coast of Thailand and Cambodia, and small islands in the Philippines, Fiji, etc.

7. Set a low spending limit on your cards (and reset it often)

This is a general tip to minimize the amount of money that you can lose if your card gets compromised.

Of course, remove it if you’re going to make a big purchase. Then put it back.

Most fintech banks have it as an option somewhere in their apps.

8. Check your online banking often

I thought I was immune to getting defrauded because I didn’t input my card details on dodgy websites. Until one day, when it happened.

I hadn’t actually done anything stupid. I couldn’t figure out how 2 fraudulent transactions appeared on my balance sheet. I never found out.

Revolut support was extremely helpful and prompt in initiating the review process and refunding the money.

Another time, I had a double transaction, and it was also fixed quickly.

Once, I got incorrectly billed for a service I had canceled. I also sorted it easily, helped by the app’s support.

I have made it a habit to check my money apps at least once a week, sometimes even more often. You should, too.

9. Never have all your cards in one place

For obvious reasons, don’t keep all your cards in your wallet. Have at least one hidden in your backpack.

10. Always pay in the local currency

In places where 2 prices are listed, one in the local currency and one in USD/EUR, always pay in the local currency.

The exchange rate favors the vendor. They are providing a service (i.e., letting you pay in USD) and are charging for it. You will always, always, always pay less if you pay like a local.